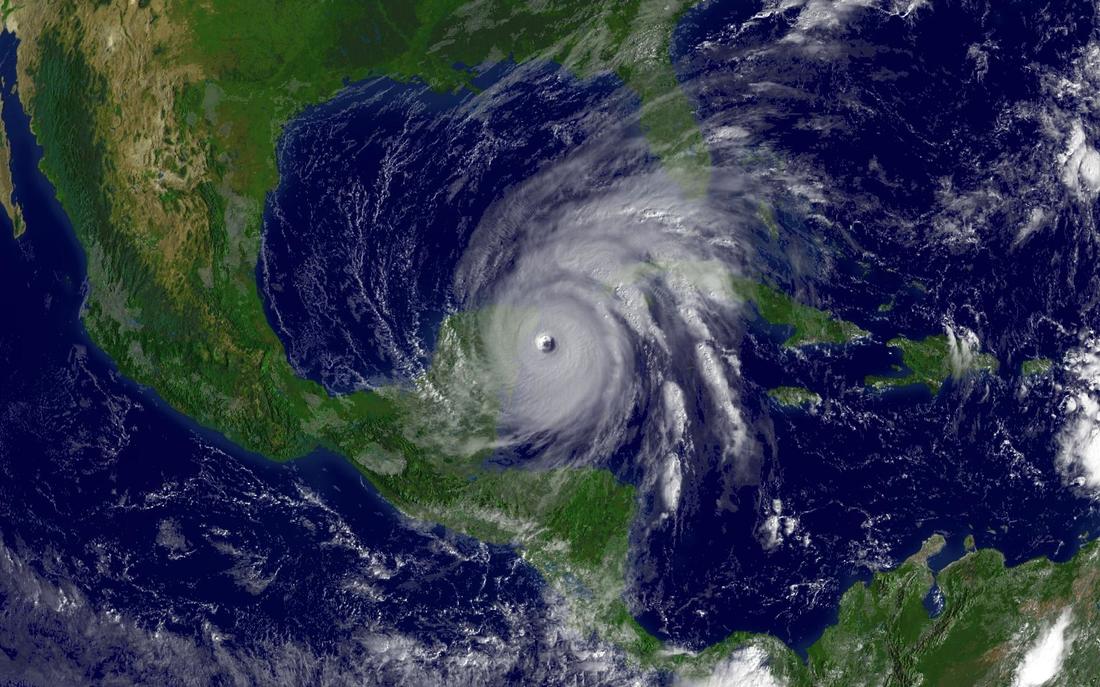

Can you accident proof your vacation? As most of you are aware, I not only work in the travel industry as an agency owner, but I’m also an avid traveler myself. I absolutely love to travel. Travel stretches you, enriches your life, teaches you about other countries, people, and cultures. But we live in an imperfect world where sometimes bad things happen. What do you do when unexpected disaster strikes while on a trip? Who will you call for assistance, a medical care flight out, or to find out what to do since you’re going on your third day without your luggage and the airline doesn’t have any answers for you? First, you call me, your travel professional. Second, you call your travel insurance provider. Travel insurance. Consumers seem to have a love hate relationship with it. Is it a necessary evil? Is it just a way to try to squeeze more money out of you after you’ve already spent so much on your actual vacation? Or, is it a mandatory prerequisite that no traveler should go without? I strongly believe it is the third option, and let me explain to you why.  Eight years ago, my husband and I took our three lovely children to Uganda for what was meant to be a 10-day trip. The children were ages 5 months, 2, and 7. My husband and I were much younger (and healthier). He was in school at the time working on his Master’s degree and we didn’t have a ton of expendable income. But we bought that travel insurance policy. And we are so thankful we did. You see, accidents happen. That’s why they’re called ACCIDENTS. You can’t foresee them, prepare for them, or avoid them. How were we to know that less than 24 hours after arriving in Uganda my husband’s appendix would decide it was the perfect time to require surgery and removal? Seriously, he had to go all the way to Africa to have an appendectomy. What should have been a simple surgery ended up turning into him having his entire abdomen cut open because of complications. Did I mention we were in Africa? In an open-air hospital where he had got to sleep under a mosquito net? Yeah. Did you know that in many countries hospitals will “hold you hostage” until you pay your bill (preferably in cash with local currency) and not you leave until you do? Truth. So, what was supposed to be a 10-day trip turned into a five week stay requiring complete re-booking of international airfare for the five of us, with my husband in First Class because of his physical state. They almost had a nurse fly with us. And guess how much all that cost our family. Nothing but the price of the policy. But the comfort in knowing that financially it would all be taken care of, and that they had a medical helicopter ready to care flight him to South Africa for emergency care if things went South is truly priceless. I recognize this is an extreme example, and many people ask what the chances of that really are. I don’t know. What are the chances? And does it matter? Is it worth saving a few hundred dollars after you’ve more than likely invested thousands in your vacation? There are many other things that travel insurance covers. It isn’t just medical emergencies (though those can tend to be the most costly and unexpected). Coverage, depending on your carrier and policy, can include trip cancellation, flight delays, and lost and delayed luggage.  Remember I went to France just this past March. I was traveling through the New Aquitaine region and Basque country attending numerous hosted dinners, meetings, and events. I was also totally and utterly without my luggage for 5 of those days. 5 days. No luggage. Work trip. But I was covered. I had purchased the trip insurance. I was able to shop and purchase clothing for each day as needed, and after I got home I submitted my claim and receipts to my insurance company and received a full reimbursement. As you can see, I am a huge proponent for trip insurance. I strongly encourage each and every one of my clients to purchase a policy. In fact, if they don’t, I have them sign a waiver stating that they were offered the insurance for purchase and opted not to purchase it. Legally, I must protect myself and my business from someone coming back (usually after some sort of issue arises on their trip) and trying to hold me liable. Yes, sadly, it has happened. I cannot control the weather and grounding of your flight, or if a hurricane will change course and head straight for your island resort destination or cruise ship. The insurance waiver form simply puts that responsibility back on you, the traveler and client. You’re big. You can make your own choices. I can advise you and offer my recommendations, but ultimately the choice is yours. So, what will it be? Are you feeling lucky? Gonna roll those dice or play it safe? It really is up to you. I hope you will choose to protect yourself, your loved ones, and your investment. Because remember, life is short. Stop Dreaming. Start Going.

0 Comments

Leave a Reply. |

It's all small world, after all - let me help you see it all. Archives

June 2020

Categories |

RSS Feed

RSS Feed